News

Read Our Latest Posts

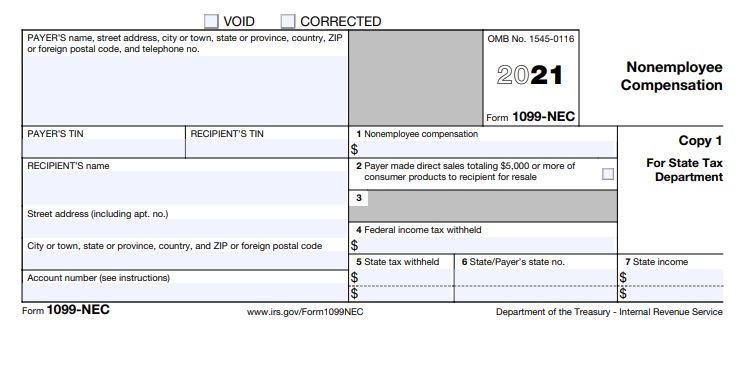

1099-NEC Joins Combined Federal State Filing Program TY2021

October 18, 2021

During the 2020 tax year, the Internal Revenue Service (IRS) added Form 1099-NEC: Nonemployee Compensation. The form is now in its second year since its re-introduction, and the government agency is including it in the Combined Federal State Filing Program (CF/SF). Making Filing Easier Recently, the IRS released Publication 1220 confirming that it has included ... 1099-NEC Joins Combined Federal State Filing Program TY2021

Tab Service Company Delivers Fast and Efficient Accounting Services

May 18, 2021

When it comes to state taxes, the term 1099 form is something predominantly heard. For many people and businesses, dealing with 1099 forms and accounting, in general, can be immensely overwhelming. For that reason, our team at Tab Service Company is here to help! For decades, Tab Service Company has been providing accounting support to ... Tab Service Company Delivers Fast and Efficient Accounting Services

Scam Targeting University Students and Staff

April 5, 2021

University students and staff should be aware of IRS impersonation email scam People should be aware of an ongoing IRS-impersonation scam that appears to target educational institutions, including students and staff who have .edu email addresses. The suspect emails display the IRS logo and use various subject lines, such as Tax Refund Payment or Recalculation ... Scam Targeting University Students and Staff

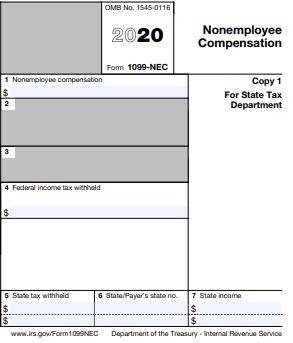

1099-NEC State Reporting Requirements TY2020

December 15, 2020

The 1099-NEC will not be part of the IRS Combined Federal State Filing Program for TY2020. If you have an obligation to report 1099-NEC directly to states, you should follow the instructions below when formatting your 1099-NEC file: Populate Box 5 State tax withheld if there is an amount to report. Populate Box 6 State/Payer ... 1099-NEC State Reporting Requirements TY2020

Seven Best Practices as You Navigate 1098-T Files

December 3, 2020

This is a guest blog post, originally featured at Nelnet Campus Commerce: campuscommerce.com/seven-best-practices-as-you-navigate-1098t-files/ In Brief: Outline of seven essential tips to when navigating 1098-T files Highlight of common errors institutions experience while processing 1098-T’s and insights on what is a qualified payment Nelnet and the TAB Service Company have been partners for four years Best ... Seven Best Practices as You Navigate 1098-T Files

CARES Act and Funding for Students

August 19, 2020

How will Coronavirus stimulus benefit students? COVID-19 has impacted all sectors and industries, and education is no exception. On March 27, 2020, CARES, or Coronavirus Aid, Relief, and Economic Security Act, provided federal stimulus aid to the Department of Education to supplement institutions and students with COVID-19 pandemic related expenses and financial needs related to ... CARES Act and Funding for Students

1099-NEC to be Reintroduced in 2020

August 8, 2019

The IRS announced that it will be bringing back form 1099-NEC to report non-employee compensation separate from the 1099-MISC. This form 1099-NEC has been retired since 1983. The change would go into effect for TY2020 (not the current 2019 tax year). Since the PATH Act was passed in 2015, it effectively created two filing deadlines ... 1099-NEC to be Reintroduced in 2020

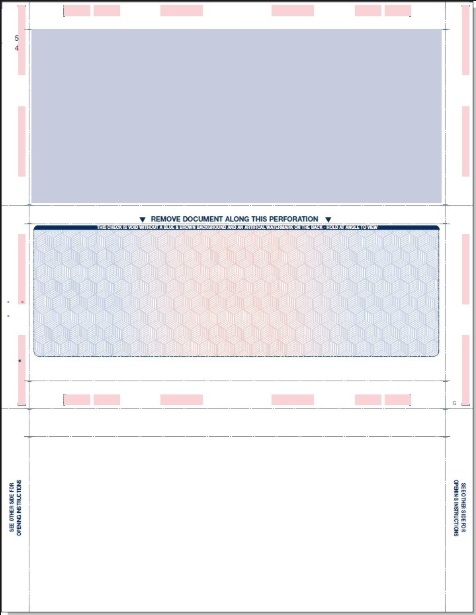

Pressure Seal 101

August 15, 2018

You may not be familiar with what pressure seal forms are but, the chances are that you have come into contact with them before. Most often pressure sealed forms are used to print and mail tax documents, checks, grade reports, invoices or financial statements. They have been the go-to option for high-volume mailers because they ... Pressure Seal 101

What you need to know about GDPR

May 14, 2018

Chances are likely that you have heard the acronym GDPR in recent news headlines. But, what exactly is this regulation and how does it impact businesses outside of the European Union? The General Data Protection Regulation (GDPR) legislation was created back in April 2016 and is scheduled for implementation later this month (May 25th, 2018). ... What you need to know about GDPR

Affordable Care Act Penalties: Letter 226J

April 10, 2018

The Affordable Care Act (ACA) filings started in tax year 2015 and the reporting has been ongoing. The applicable large employers (ALE’s) that have been required to file the 1095/1094-C haven’t seen any penalties until recently. The penalty assessment notice from IRS is called 226J and it is sent to ALE’s who the IRS believe ... Affordable Care Act Penalties: Letter 226J

1098-T REPORTING – BOX 1 REPORTING NOT REQUIRED IN TAX YEAR 2017

May 3, 2017

When the PATH Act of 2015 was introduced the IRS required that colleges and universities report the amounts received instead of amounts billed for qualified tuition and related expenses. However, the IRS met quite a bit of push back from institutions that were now faced with huge administrative challenges to change their accounting systems to ... 1098-T REPORTING – BOX 1 REPORTING NOT REQUIRED IN TAX YEAR 2017

Does ACA repeal = No more IRS reporting requirements?

March 20, 2017

With headlines trending on the repeal of the Affordable Care Act (ACA) a lot of employers are wondering….Will I still have to report employee health coverage to IRS next year? In short the answer is yes and employers will more than likely have to continue reporting for quite a while. Here’s why…. The new bill ... Does ACA repeal = No more IRS reporting requirements?